Inkwell Capital Test

Thinking of Taking a Loan from Your 401(k) Plan? Just Don’t Do It

You may have heard in the news recently that the current bull market is now the longest in history. The S&P 500 index has not had a 20%-or-more decline since hitting its most recent low in early March 2009. In other words, the stock market has been going mostly up for at least 3,450 consecutive days now.

If you have a significant portion of your 401(k) account invested in stocks (and you should, as we have discussed in other articles), this means the balance in your account may have become a bit swollen. In case you have been tempted to tap into that largesse in the form of a 401(k) loan, we would like to offer you one word of advice about that:

Don’t.

Could You Please Elaborate?

But perhaps if we could elaborate a bit on that, our advice might be a little more helpful. For instance, you may not have even known that taking a loan from your 401(k) was even an option. And depending on the size of your employer, it may or may not be. The Employee Benefit Research Institute estimates that 90% of employers with 1,000 or more employees do offer 401(k) loans, but for smaller companies it may not be an option. For those of you who could take advantage of it, here is how it would work:

If you are in a situation in which you are in need of more cash than you have readily available, then you may consider taking money out of your retirement account to tide you over until better times. Taking an actual distribution from your 401(k) balance would cause you to owe income tax to the IRS for the amount you withdraw, and it may also subject you to a 10% penalty if you are not yet 59-1/2 years old. However, 401(k) loans definitely avoid the 10% penalty and technically avoid being assessed income tax.

(One quick aside: a 401(k) “loan” is not actually a loan. You don’t have to pass a credit history check before taking the money, and it does not affect your credit score. But it is borrowing money that needs to be paid back, so it’s easiest to simply to refer to it using the word “loan.”) Other real loan options would be carrying a balance on a credit card or asking a local bank for a personal or home equity loan. Usually, 401(k) loans have interest rates lower than both of those, though.

Wait a minute, all these data points seem to be saying that 401(k) loans are great: low interest rates, no tax consequences, and no penalties? Sign me up!

But Wait, There’s More

So far we’ve only covered the benefits. There are significant drawbacks too, and we believe they far outweigh the good stuff.

First, some 401(k) plans do not allow their participants to add any new contributions for a while after taking a loan. This period could be up to six months, which means that you could lose (a) the ability to make half of your annual contribution to the plan, (b) access to half of your employer’s matching contribution if it’s dependent on what you put in, and (c) the means to shield a significant portion of your income from current income taxes.

Second, depending on what the stock market does during the time your loan is outstanding, you could be hindering your retirement. Let’s say you take a loan of $25,000 from your 401(k) balance and then repay it in full one year later. If the stock market has a banner year, and goes up say 20%, you could be depriving yourself of a tax-deferred $5,000 “bonus” in the form of foregone performance.

Third, remember how earlier we said that income tax is not technically assessed on 401(k) loans? Well, that is true: the money that a person withdraws from their 401(k) in the form of a loan is not reported to the IRS as taxable income. However, loans must be repaid. And the dollars used to repay 401(k) loans will have already been taxed by the IRS. So yes, when the money comes out of the plan for the loan, it is not technically taxed. But the dollars that repay the loan are taxed, and will be taxed again when they are withdrawn during retirement, so this effectively negates one of the features of a 401(k) loan that, on first glance, seemed like a benefit.

Fourth, it’s possible that one of the other ostensible benefits of a 401(k) loan may end up disappearing as well, and that’s the avoidance of the 10% early withdrawal penalty. Most 401(k) plans that allow loans say that the loans must be repaid by the sooner to occur of two events: either when the participant leaves their job, or after five years have elapsed. If the loan is repaid before the sooner of those two events, then the IRS considers the loan to have been just that: a loan. But if one of those events occurs without the full balance of the loan having been satisfied, then the IRS will consider the loan to have actually been a withdrawal. Withdrawals from a 401(k) are considered taxable income, and they are subject to the 10% penalty if they were made before the participant turned 59-1/2 years old.

Why Would Anyone Do It?

This is starting to seem like a no-brainer. A 401(k) loan deprives its taker of any market gains that happen during the life of the loan, possibly restricts his ability to contribute to the plan and shield those contributions from income tax, is effectively taxed at the marginal income tax rate since the dollars used to repay the loan have already been taxed, and could also be assessed a 10% early withdrawal penalty.

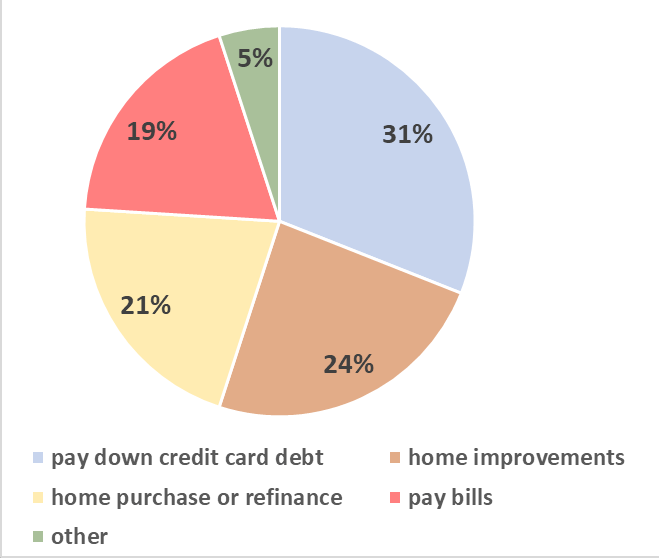

So why would anyone still do it? According to a study done by Fidelity Investments, the most common reasons for 401(k) loans are reported to be:

These are the self-reported reasons for people taking 401(k) loans, which may or may not match up exactly with what the actual reasons were. For instance, some financial planners report hearing tales of people using 401(k) loans in order to install a back-yard swimming pool or taking a particularly lavish international vacation.

Hopefully we can all agree that it would be silly to possibly de-fund your retirement account in order to pay for a luxury that you don’t need. So please don’t ever do that.

Even these self-reported reasons, which may seem on their surface to make financial sense, don’t hold up to our way of thinking. For instance, if a person has a stubbornly high credit card balance, there are cheaper ways of dealing with that than using a 401(k) loan. The simplest would be to simply apply for a new card with a lower interest rate and a balance-transfer option. Some of the balance transfer offers we have seen lately entail 0% interest rates for the first 12 or 18 months. A person could rotate from card to card over the years, kicking the can down the road so to speak, until the balance eventually gets wiped out.

Or if a person desperately wants a new kitchen but doesn’t have the cash on hand to pay for it, they could instead use a home equity loan or line of credit, which would allow them to bypass the real and potential drawbacks of a 401(k) loan.

Basically, it all boils down to patience. A retirement plan such as a 401(k) is designed to help you fund your retirement, which could be years or even decades from now. The whole system is designed to reward your patience. So don’t counteract that with the impatient act of tapping into your 401(k) “piggy bank” before it’s actually time to retire.

With all that said, we do want to at least recognize that there could possibly be a good reason for accessing 401(k) money early. Perhaps a person could be hit with large and unexpected medical expenses, for instance. Or maybe a person has stretched themselves too thinly, and they are a whisker away from declaring bankruptcy. But if something like that were to come along, then the person would probably be more interested in a hardship distribution and not a loan. Which is a topic for another article.

So let us recap as succinctly as possible our advice for whether you should ever take a loan from your 401(k) retirement plan:

Don’t.